H & S Real Estate Group

Looking for clarity on the Underused Housing Tax (UHT)? For years, this one-percent federal levy has been a complex, confusing headache for Canadian & foreign property owners, second-home owners, and real estate investors alike.

It wasn’t just the 1% tax on vacant properties that caused stress; it was the bureaucratic nightmare of filing the underused housing tax return. Even if you were exempt as a Canadian citizen, the confusing paperwork, the vague definitions, and the threat of massive non-compliance penalties turned a simple annual formality into a source of constant anxiety. Thousands of Canadians who owned a cottage or a second rental unit were forced to spend money on professional advice to avoid fines that could run into the thousands of dollars. You were stuck wondering: Do I need to file? Did I miss a deadline? Is this one property going to cost me thousands in fines?

The anxiety is finally coming to an end. The federal government has listened to industry demands and, with the tabling of Budget 2025 on November 4, 2025, announced plans to officially eliminate the Underused Housing Tax starting in 2025. The House of Commons approved Budget 2025 on November 17, 2025.

In this post, we break down what this significant change means for you, and when you can officially stop worrying about the annual filing deadline and the final steps needed to make this complicated tax a thing of the past.

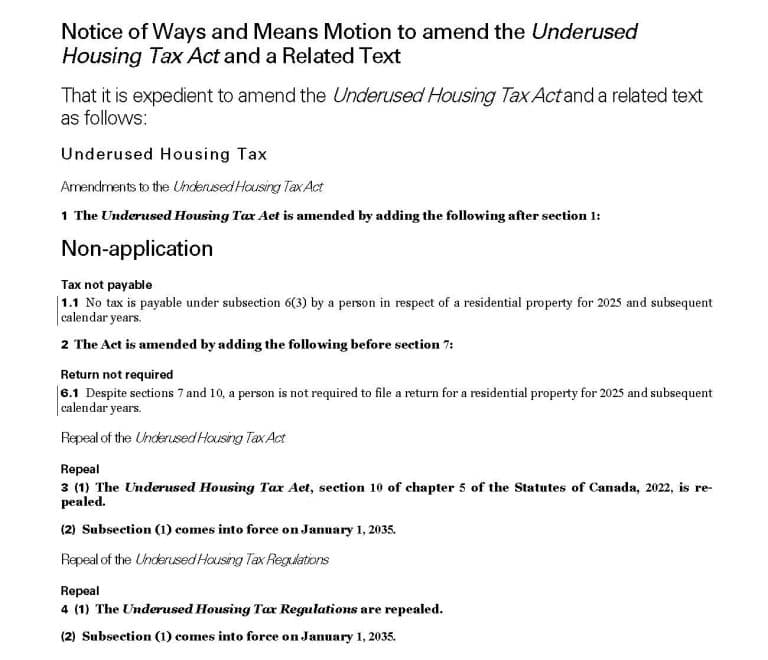

Source: Page 403, Budget 2025

Table of Contents

That is an excellent and essential question! The Underused Housing Tax (UHT) has been a significant point of confusion and compliance stress for many property owners across Canada since its introduction.

The UHT is an annual 1% federal tax on the value of vacant or underused residential properties in Canada.

The UHT is mainly aimed at Non-Resident, non-Canadian owners of residential property in Canada. However, the reason for the widespread confusion is that the law divides owners into two categories that determine their obligations:

These owners generally have no UHT obligations (no need to file a return or pay the tax). This group includes:

These owners must file an annual UHT return (Form UHT-2900) for every property they own, even if they qualify for an exemption and owe $0 in tax. This group includes the tax’s intended target, non-Canadians, but also includes certain Canadian citizens or permanent residents if they own property in a specific way:

It was the requirement for Canadian trusts, partnerships, and private corporations to file an annual return—even when exempt from paying the tax—that caused the most compliance anxiety and led to significant late-filing penalties for many Canadians.

The Underused Housing Tax (UHT) filing deadline for the 2024 calendar year is April 30, 2025. Even with the proposed cancellation for 2025, Affected Owners (including non-residents) must file their 2024 return by this date to avoid significant penalties.

The original deadline to file the 2025 Underused Housing Tax return is April 30, 2026.

However, Budget 2025 proposes to eliminate the UHT for 2025 and future years. Suppose this passes the final vote, expected on November 17, 2025. In this case, the obligation to file for 2025 will be cancelled in its entirety, and no return will be required on April 30, 2026.

Failure to file the UHT return by the deadline incurs severe penalties, even if no tax is owed. The minimum late-filing penalty is $1,000 for individuals and $2,000 for corporations, trusts, and partnerships. Interest will also be charged on any unpaid tax amount (tax payable). File on time to avoid these significant, mandatory fines. See the table below for the prescribed interest rate.

| Year | 1st Quarter | 2nd Quarter | 3rd Quarter | 4th Quarter |

|---|---|---|---|---|

| 2025 | 8% | 8% | 7% | 7% |

| 2024 | 10% | 10% | 9% | 9% |

As mentioned earlier, the Canadian federal government, in its Budget 2025 proposal, has announced its intention to eliminate the Underused Housing Tax starting in the 2025 calendar year.

This means that if the budget passes:

This measure is being taken due to the UHT’s complexity, its high administrative burden, and the existence of similar provincial and municipal vacancy taxes (such as those in BC and Toronto). See below for other similar taxes in different provinces:

British Columbia

Ontario

The budget is currently progressing through the legislative process, which includes a speech by the Finance Minister on Tuesday, November 5, 2025, followed by four days of debate (including November 5, 6, 7, and 17). The final vote on the budget, which contains the measures to eliminate the UHT, is scheduled for November 17, 2025.

While the Canadian government’s proposal to end the UHT is excellent news, the final details and legislative approval are still pending in Parliament. You need real-time, confirmed information to make wise decisions about your investment property or bare trust. Don’t wait for the news to break—be the first to know. Subscribe to our newsletter today to receive a UHT status alert the moment the bill passes, along with expert guidance on how this change affects your 2025 filing.

The cancellation of the Underused Housing Tax (UHT) was proposed in the Canadian Federal Budget on November 4, 2025. The 2025 Budget proposes eliminating UHT from the 2025 calendar year onward. As a result, there will be no requirement to file UHT returns, and no UHT will be payable for 2025 or any subsequent years. However, all UHT requirements for the years 2022 to 2024 will still apply, including any associated penalties and interest.

During the House of Commons debates on November 5, 2025, there was no mention of cancelling the underused housing tax in the House of Commons proceedings. The discussions in Question Period focused more on broader budget issues, government spending, tax policies, healthcare, and economic concerns. There was no specific reference to the cancellation of the underused housing tax.

During the House of Commons debates on November 6, 2025, Member of Parliament Adam Chambers, speaking against the new federal budget, highlighted the proposed elimination of the Underused Housing Tax.

He categorized the UHT cancellation as one of several major “reversals” of the previous government’s policies, alongside the removal of the digital services tax and the luxury tax. Chambers argued that the Liberals should not receive praise simply for undoing the “damage” and failed legislation they initially implemented, asserting that the UHT’s removal is a retraction of a failed policy rather than a new achievement.

During the House of Commons debates on November 7, 2025, the Underused Housing Tax was not mentioned specifically.

However, the discussion was heavily centred on general themes of housing and taxation. Key housing points included the affordability crisis, the government’s proposal to eliminate GST for first-time buyers on homes valued at $1 million or less, and launching the “Build Canada Homes” initiative. Various other taxes were debated, such as high overall taxation, hidden food taxes, and the scrapping of the luxury tax on certain high-value items, including private jets and yachts.

During the House of Commons debates and vote on November 17, 2025, Budget 2025 was approved.

Canada’s 2025 federal budget has eliminated the Underused Housing Tax (UHT) starting with the 2025 tax year, following the budget’s narrow passage in Parliament. This means real estate owners will no longer need to file UHT returns or pay the tax for 2025 and future years, reducing compliance costs and uncertainty for investors and homeowners. However, UHT obligations for the years 2022–2024 remain in effect, so returns and payments for those years are still required. The move supports housing market stability and makes Canadian properties more attractive for buyers and non-residents.

Sam Huang PREC

H & S Real Estate Group

Real Estate Coal Harbour

RE/MAX Select Properties

Address: 5487 West Boulevard, Vancouver BC V6M 3W5, Canada

Phone: 778-991-0649

WeChat: ubchomes

QQ: 2870029106

Email: Contact Me